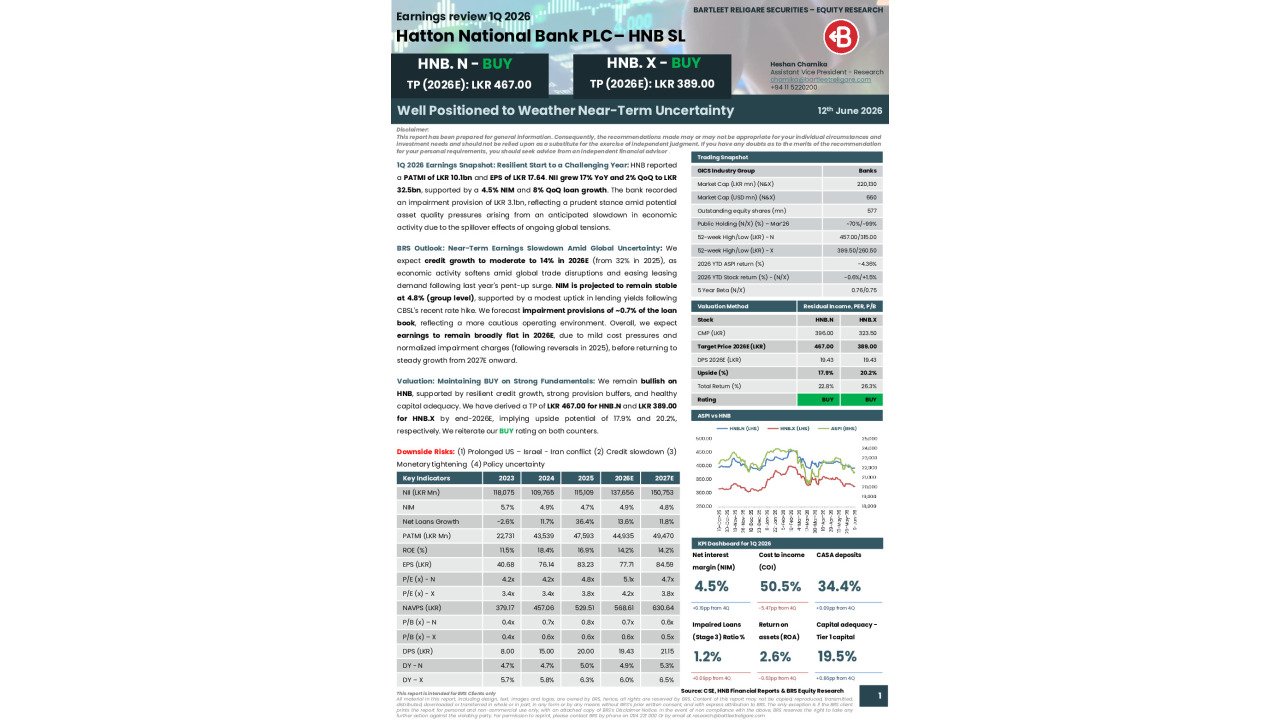

ACL Cables PLC - BRS Earnings Review 4Q FY26

Loading...

Earnings Reviews

30/06/2026

262

0

📈 ACL 4Q FY26 Earnings Review

Near-Term Earnings Outlook Aided by Price Revisions and Stable Demand

• PATMI rose 22.4% YoY to LKR 1.6bn as revenue increased 23.4% YoY to LKR 12.2bn, driven by higher volumes.

• 📉 Margins softened (GP: 19%, EBIT: 18%) on elevated raw material costs, despite stronger other income and finance income.

• 💡 Price revisions from 1Q FY27E are expected to drive a gradual margin recovery.

• 🏗️ Government & institutional demand remains resilient, while retail demand is expected to improve gradually.

Valuation & Recommendation: BUY | TP: LKR 138.00 (+37.7%)

Discussion (0)

Latest Reports

Related Reports

Free

You must login to post a comment.