COMB 4Q 2025 Earnings Review - BRS Equity Research

Loading...

Earnings Reviews

24/03/2026

406

0

📈 Built to Withstand, Positioned to Grow

💰 Strong 4Q performance: PATMI of LKR 12.9bn and EPS of LKR 7.82, with NII up 29% YoY (+8% QoQ) to LKR 37.5bn, supported by a solid NIM of 4.5% and loan growth (+10% QoQ).

📘 Cautious credit outlook: ~LKR 560bn disbursements (+37% YoY) in 2025, however loan CAGR revised to 12.4% (2025–2027E) amid external headwinds.

🛡 Asset quality improving: Stage 3 ratio at 1.5% with provision coverage at 73.5%, supporting strong buffers.

📉 Cost efficiency: Cost-to-income ratio expected to remain below 30%.

📈 Valuation & recommendation:

• COMB.N – BUY | TP: LKR 242 (+20%)

• COMB.X – HOLD | TP: LKR 210 (+11%)

⚠ Risks: Prolonged US – Israel - Iran conflict, credit slowdown, monetary tightening, policy uncertainty

Discussion (0)

Latest Reports

Free

Related Reports

Free

Free

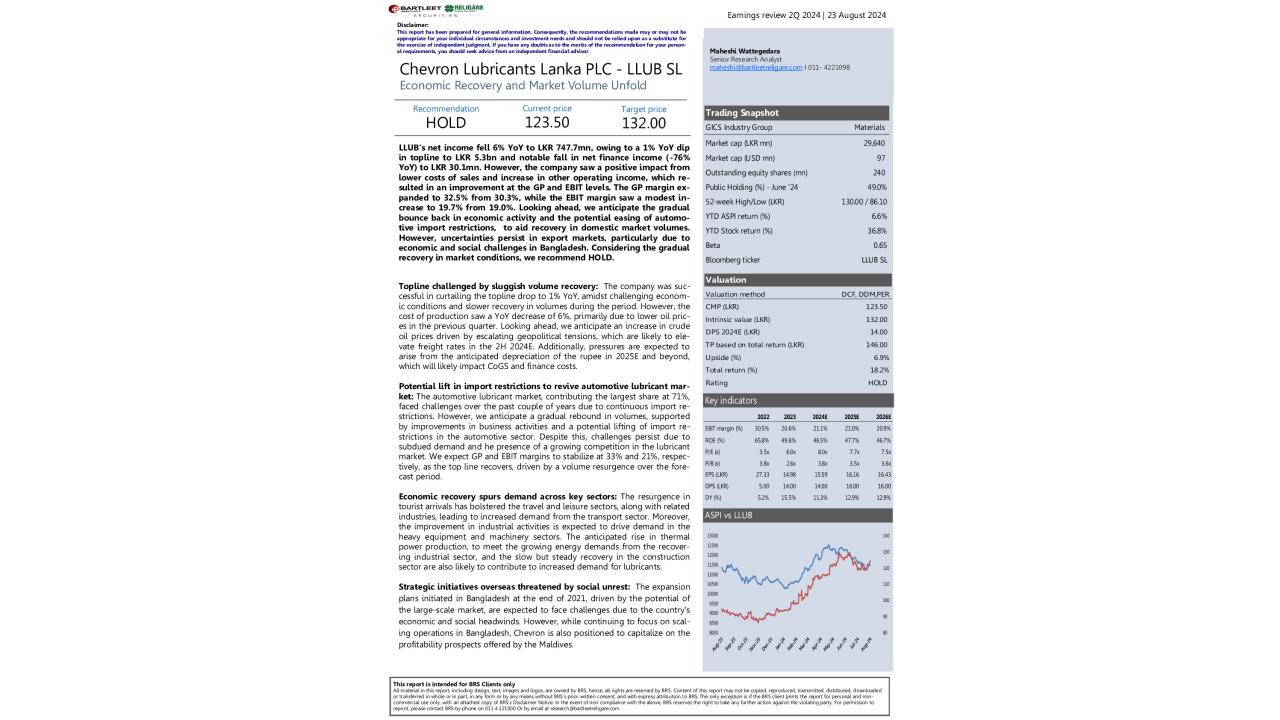

Chevron Lubricants Lanka PLC (LLUB SL ...

Economic Recovery and Market Volume Unfold LLUB's net ...

416

0

You must login to post a comment.