DFCC Information Note 1Q 2025 - BRS Equity Research

Loading...

Company Notes

18/07/2025

564

0

🏦 Licensed commercial bank since 2015; pioneer development bank since 1955.

💰 1Q25 PATMI down 21% YoY to LKR 3.0bn – weighed by a 20% rise in OPEX & lower trading income.

📉 Impairments fell 14% YoY to LKR 1.4bn, with Stage 3 loans at 5.4% & coverage at 53.5%.

📈 Net loans grew 5% YTD, outpacing industry; Deposits up 8% YTD, CASA improved to 26.5%.

💳 NII up 5% YoY to LKR 7.4bn, driven by easing funding costs. Fee income rose 24% to LKR 1.4bn.

📊 Annualized ROE for 1Q25 at 14.6%, vs. TTM ROE of 10.7% and 5Y avg. of 8.7% 🔼

🧾 Capital buffers moderate, with 240bps on Tier 1 and 100bps on Total Capital (as of Mar’25)

📍 Wide reach with 139 branches & 5,500 ATMs | Fitch rated A(lka)

Discussion (0)

Latest Reports

Related Reports

Free

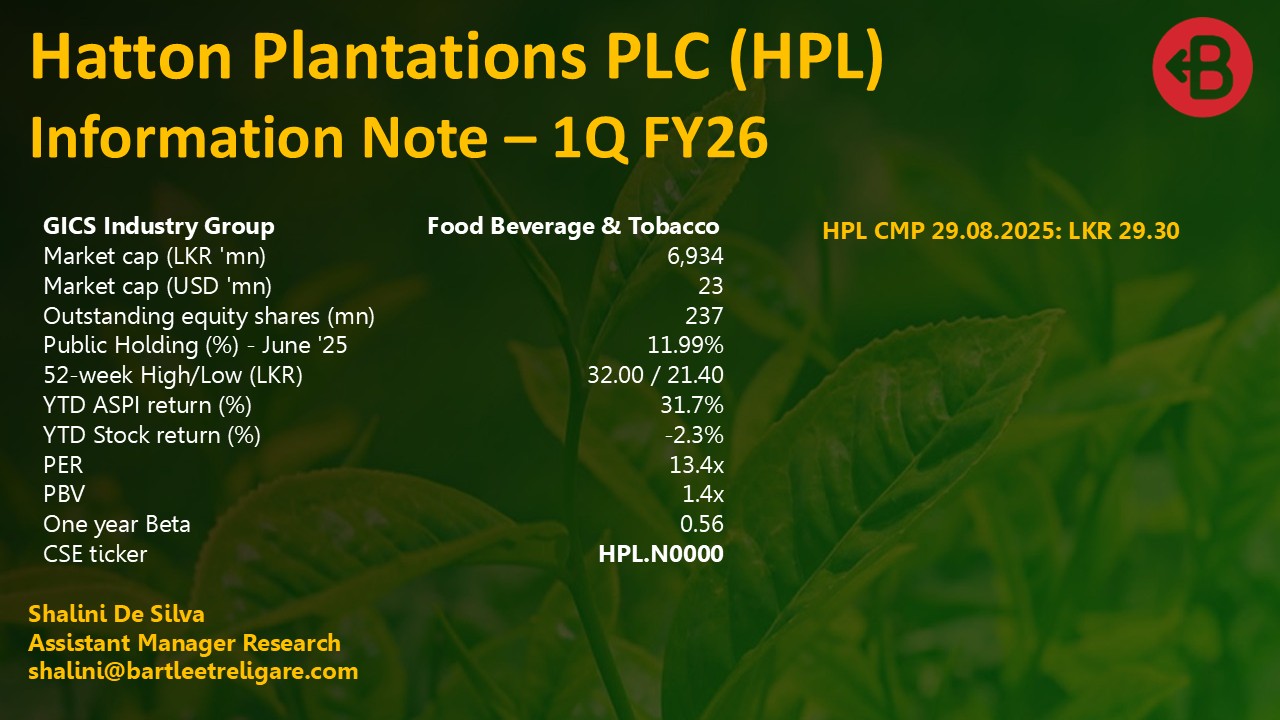

Hatton Plantations PLC (HPL) Information Note ...

Hatton Plantations PLC (HPL) Information Note - 1Q ...

260

0

Free

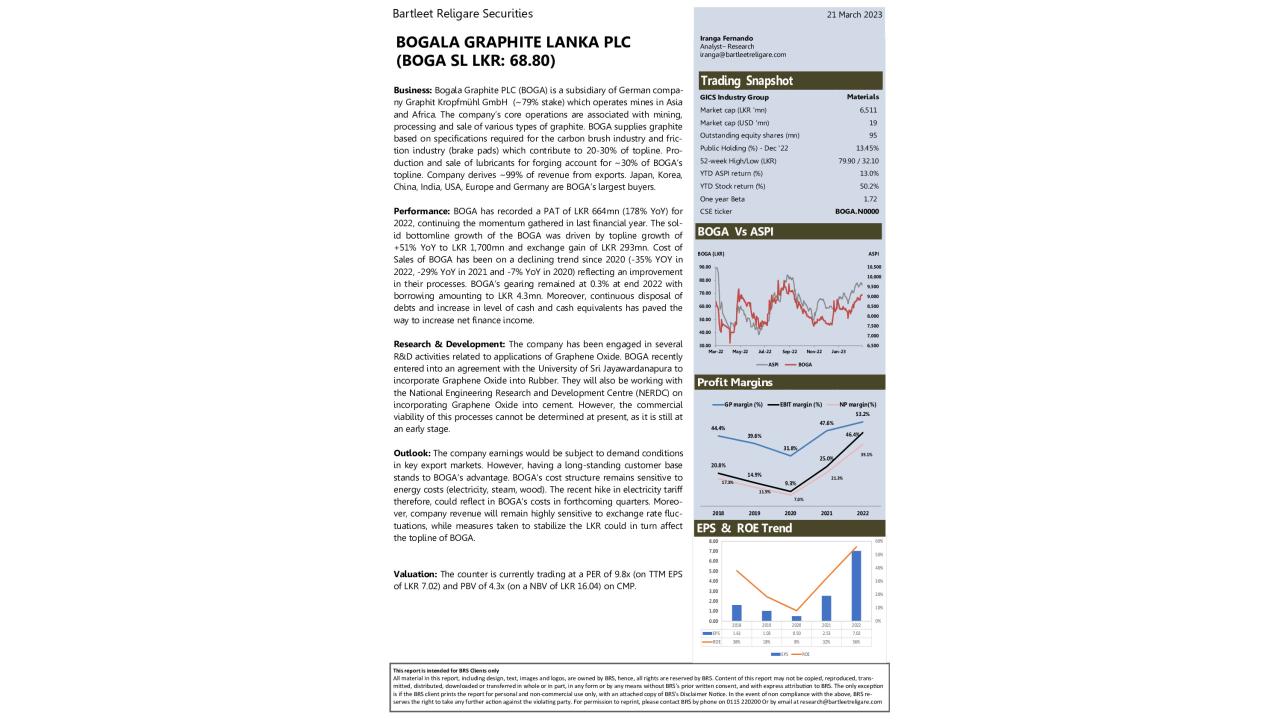

Company Information Note - BOGALA GRAPHITE ...

Company Information Note - BOGALA GRAPHITE LANKA PLC

139

0

You must login to post a comment.