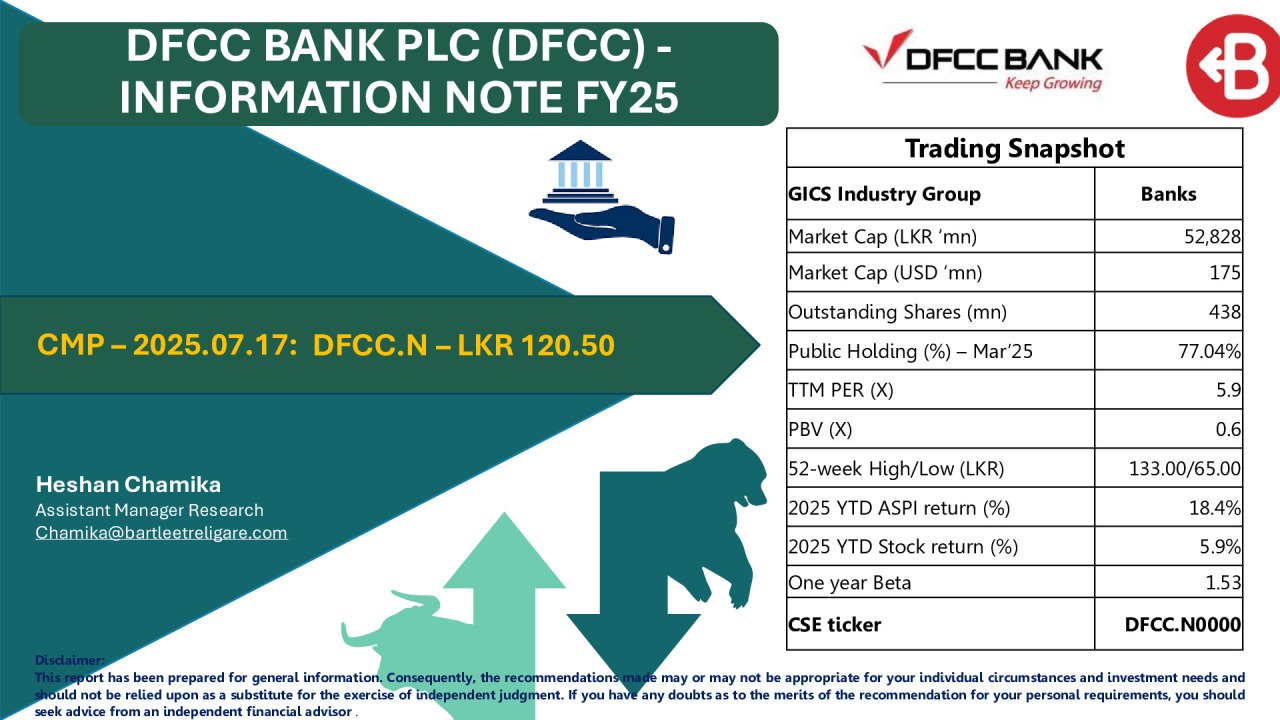

DFCC Information Note 2Q 2025 - BRS Equity Research

Loading...

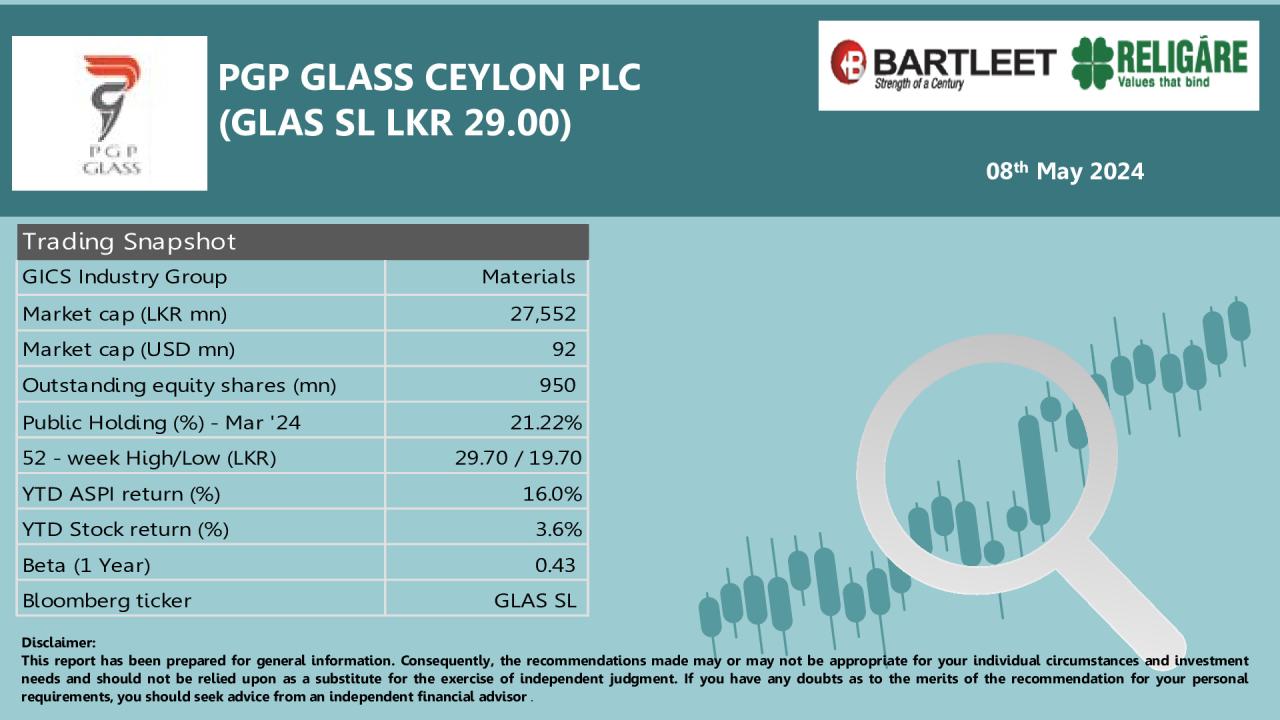

Company Notes

22/10/2025

612

0

💰 PATMI LKR 2.8bn (+51% YoY) – driven by higher NII and strong fee income, while costs stayed broadly flat YoY.

🏦 NII +16% YoY to LKR 7.8bn, aided by cheaper funding and slower rise in interest expenses.

💳 Fee & commission income +62% YoY, reflecting stronger economic and transactional activity.

🛡 Impairments +65% YoY to LKR 2.2bn, with Stage 3 ratio improving to 4.6% (from 5.7% in 4Q 2024).

📊 Loan book +17% YTD and deposits +14% YTD, outpacing listed peers’ average growth.

📈 ROE 13.4% (2Q annualized) and TTM ROE 11.2%, above 5Y avg (8.7%) but below sector avg (14%).

💹 Trading at PER 7.2x and PBV 0.7x (vs. sector avg 9.6x & 0.9x) – highlighting attractive valuations with re-rating potential.

🏆 Rated A(lka) by Fitch | 138 branches & 5,500 ATMs

Discussion (0)

Latest Reports

Related Reports

Free

DFCC Information Note 1Q 2025 - ...

🏦 Licensed commercial bank since 2015; pioneer development ...

564

0

You must login to post a comment.