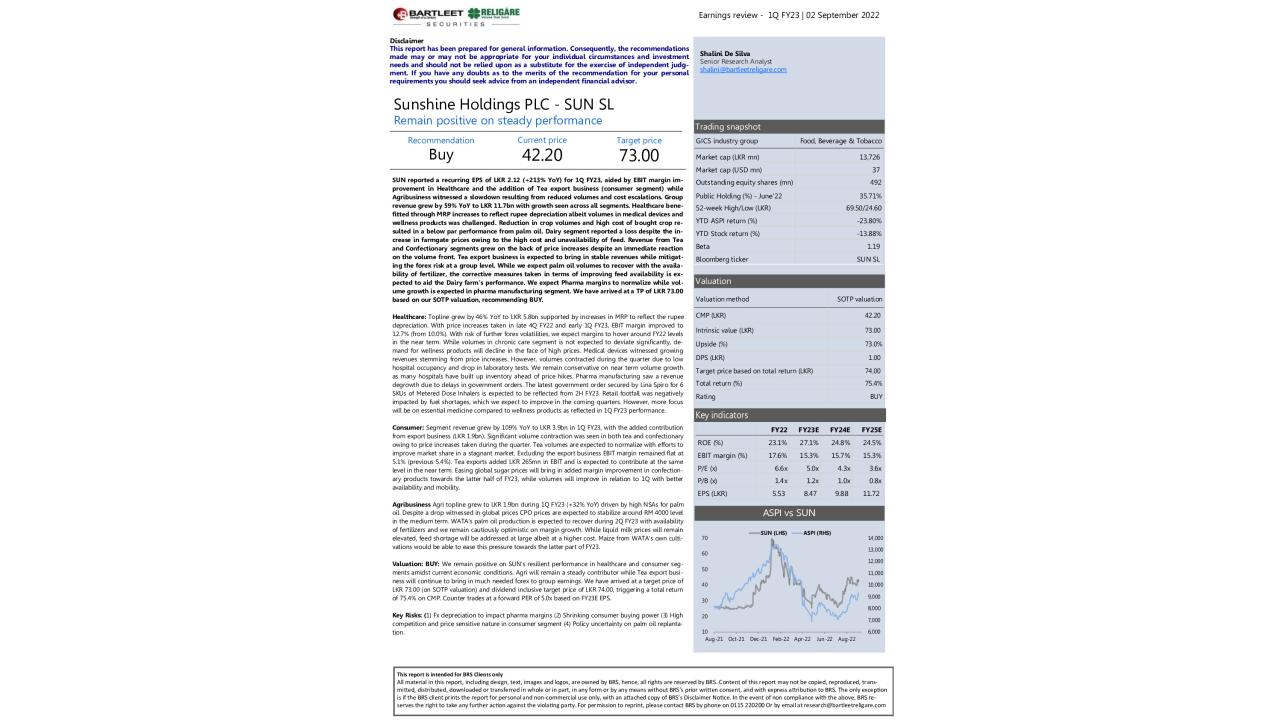

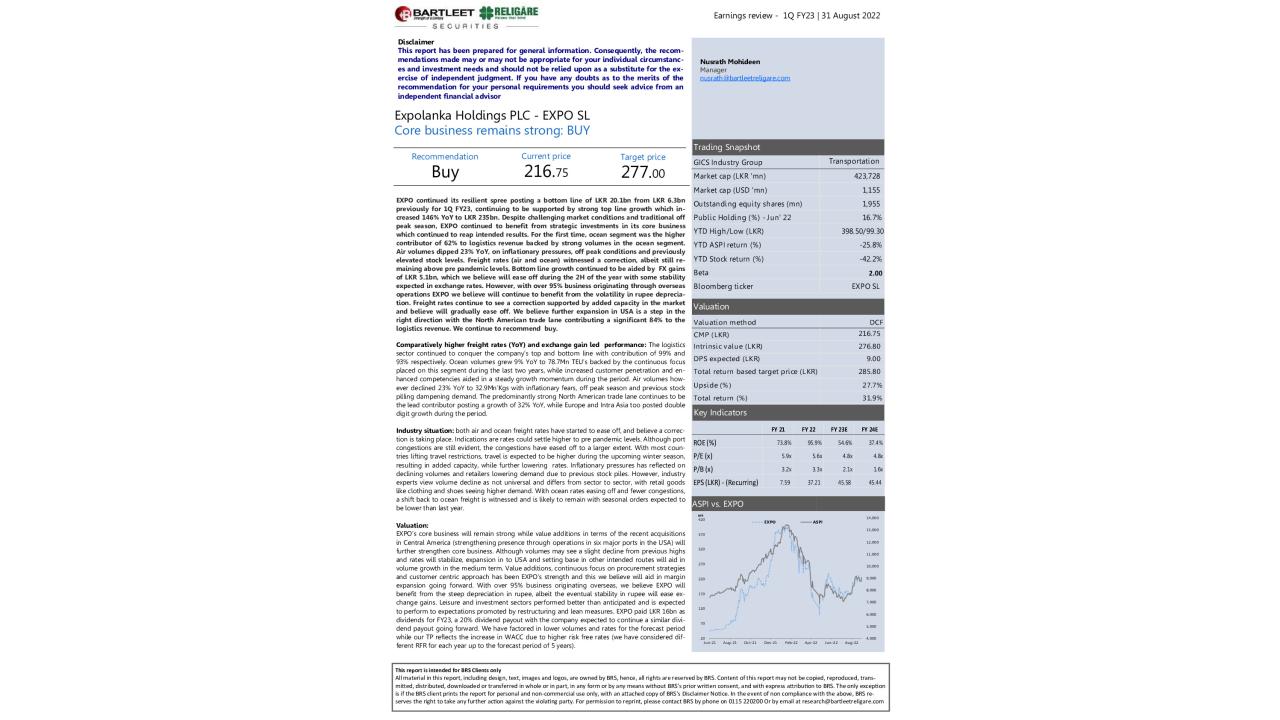

John Keells Holdings PLC (JKH) - 2Q FY25 - BUY

Loading...

Earnings Reviews

09/12/2024

496

0

JKH posted a PATMI of LKR 1.4bn in 2Q FY25 (vs. a loss of LKR 574.1mn in 2Q FY24), with an EPS of LKR 0.09 (adjusted for the subdivision). Profitability improved, supported by an exchange gain of LKR 1.9bn from WPL loan translation. Revenue grew 20% YoY to ~LKR 77.0bn, led by most sectors except Leisure. However, EBIT margin contracted to 2.0% (3.8% in 2Q FY24) due to cost pressures in Leisure and Transportation. Cinnamon Life hotels began operations in 3Q FY25, with gaming and Nuwa Hotel expected by 2Q FY26E. We remain optimistic about JKH's long-term prospects, underpinned by earnings from strategic projects and a tourism revival. Reflecting recovery momentum of economic conditions and lower interest rates, we revise our intrinsic value for JKH to LKR 25.20 (up 6.3% from LKR 23.70), incorporating rights dilution and subdivision. Recommendation: BUY.

Discussion (0)

Latest Reports

Free

Related Reports

Free

Free

TOKYO CEMENT COMPANY (LANKA) PLC (TKYO) ...

📈 Short term risks ahead, long term expectations ...

296

0

You must login to post a comment.