TILE/LWL/RCL Review - 3Q FY24

Loading...

Earnings Reviews

01/04/2024

1k

0

TILE, LWL and RCL posted considerable growth in PATMI to LKR 1.08bn (+144% YoY), LKR 1.09bn (+198% YoY) and LKR 2.96bn (+157% YoY) respectively for 3Q FY23. The growth was aided by a substantial uptick in demand during December, prompted by the increase in VAT (from 15% to 18%) coming into effect from January 2024. GP and EBIT margins hovered at similar levels QoQ, with TILE and RCL indicating improvements YoY supported by revenue growth. LWL saw higher cost escalations during the period due to the ongoing phased expansion which is to be completed by end June 2024. The decline in interest rates aided the decline in finance cost, specifically in LWL and RCL declining by 72% and 61% respectively. With import restrictions being lifted, a free flow of imported tiles in the market is evident, which may lead to an oversupply situation. Although this would lead to price competitiveness, we believe the importers and local manufacturers will have a fair market share, supported by the gradual recovery in economic conditions. We recommend Buy for TILE, LWL and RCL.

Discussion (0)

Latest Reports

Free

Related Reports

Free

Free

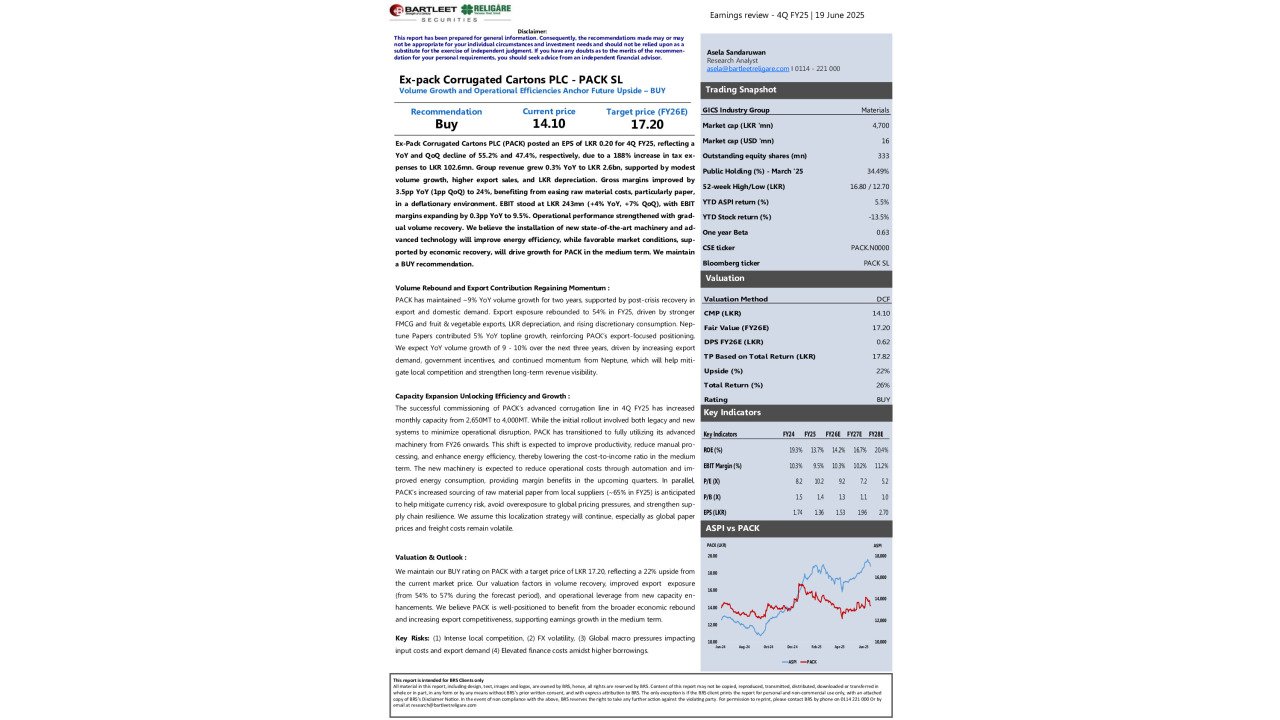

Ex-pack Corrugated Cartons PLC (PACK) - ...

Ex-Pack Corrugated Cartons PLC (PACK) posted an EPS ...

513

0

You must login to post a comment.