SFIN Equity Update - Attractive on Rights, Stretched on CMP - BRS Equity Research

Loading...

Initiation Reports

27/08/2025

383

0

Recommendation:

✅ Existing Shareholders: Subscribe to Rights ⚠️ New Investors: Growth Largely Priced-In

FY27E TP: LKR 61.00 (~9% downside from CMP)

📌 Rights Issue Strategy

Existing Shareholders – Subscribe ✍️ - Rights priced at LKR 26.50, ~130% upside.

Trade Rights Smartly 💰:

Rights Intrinsic value LKR 34.50;

sell above LKR 34.50, buy below LKR 30.00.

🔹 Aggressive Lending Growth Backed by Rights Funds

Rights issue raising LKR 2bn strengthens capital adequacy to sustain MSME-focused lending.

🏢 Branch Expansion to Target Underpenetrated MSMEs

4 new branches added in FY25; 10 more planned in FY26 for semi-urban, high-yield segments.

🛡️ Strong Asset Quality

Prudent provisioning maintains robust asset quality despite rapid growth.

💸 Valuations

Trades at forward PER 12.3x and PBV 2.0x. Forecasted ROE 20% remains attractive but largely priced in.

⚠️ Investment Risks

MSME sector exposure, rapid RWA growth, inflation-driven tightening, slower credit demand, competition from banks/NBFIs.

Discussion (0)

Latest Reports

Related Reports

Free

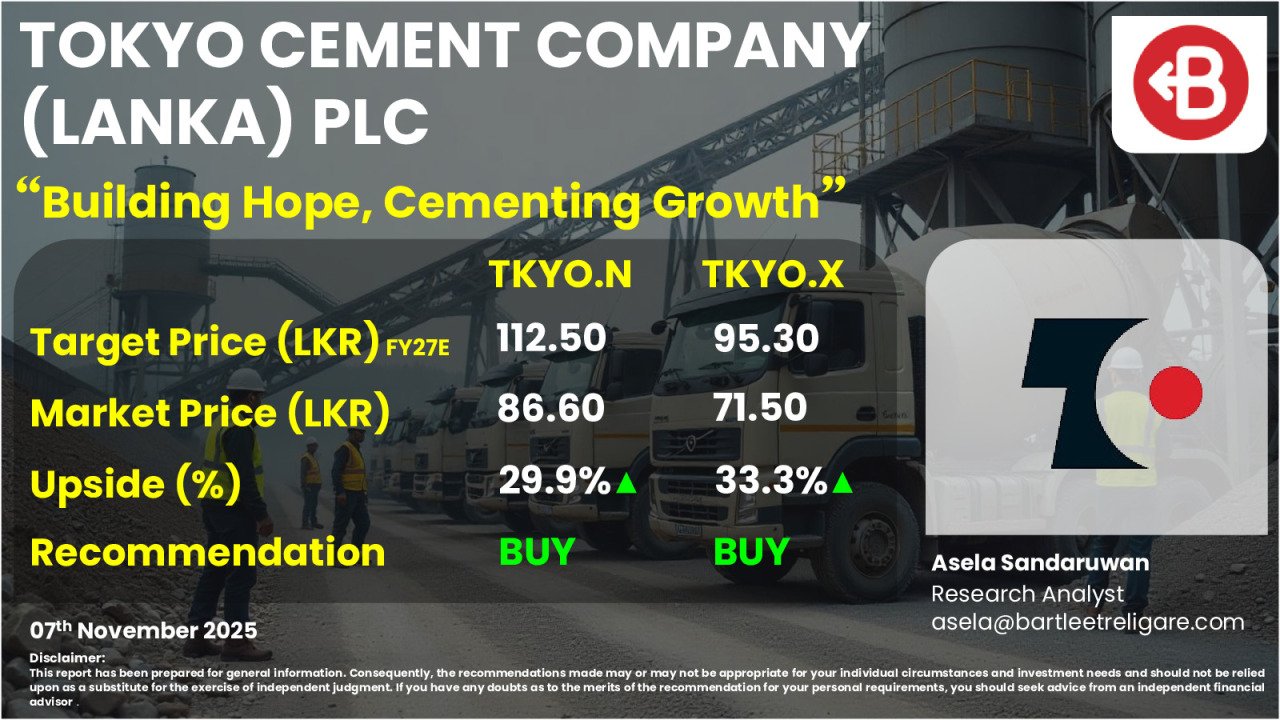

TOKYO CEMENT COMPANY (LANKA) PLC - ...

Tokyo Cement Company (Lanka) PLC (TKYO), Sri Lanka’s ...

1.4k

0

Free

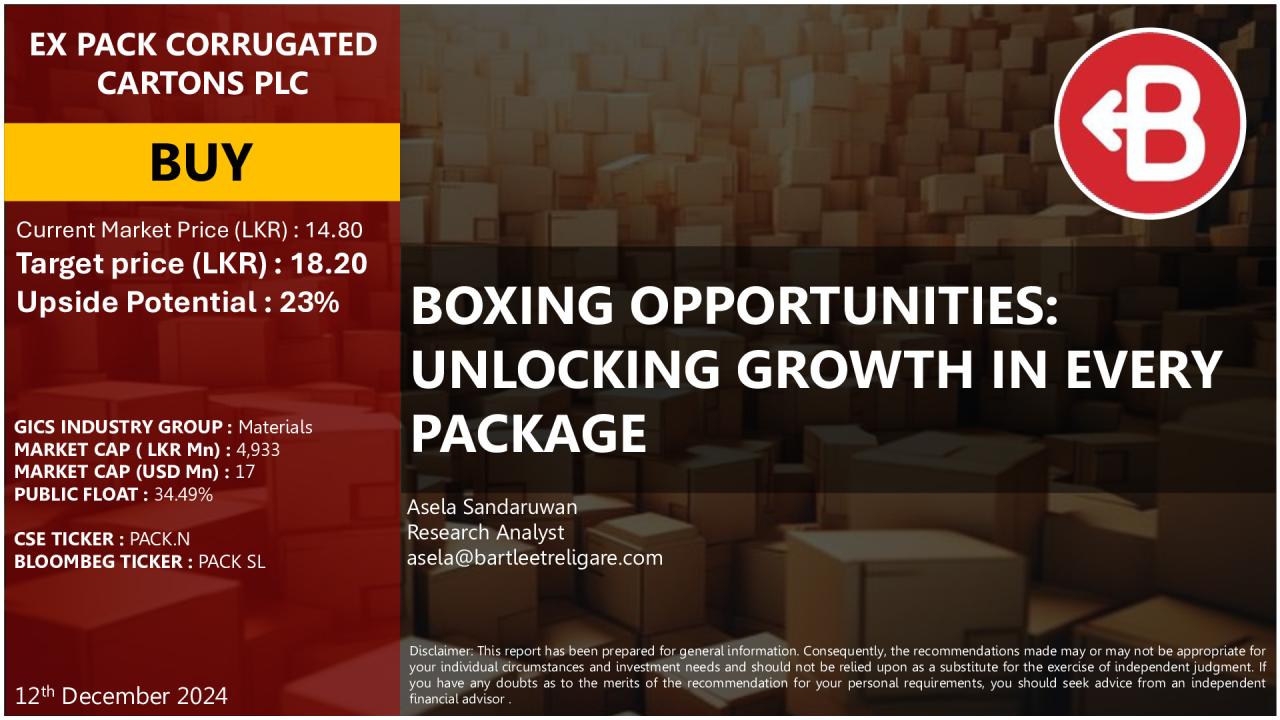

Ex-pack Corrugated Cartons PLC - Initiation

Ex Pack Corrugated Cartons PLC (PACK), a leading ...

1.1k

0

You must login to post a comment.