Sunshine Holdings PLC (SUN) - 1Q FY26: BUY

Loading...

Earnings Reviews

12/08/2025

777

0

We remain bullish on SUN’s medium to long term prospects driven by robust Healthcare segment performance. With improved manufacturing capacity Lina manufacturing is expected to grow in government orders, own brand metered dose inhalers (MDIs) and contract manufacturing for other organisations. Favourable macro conditions and recovery in Consumer spending coupled with improved Agri margins is expected to bode well for SUN’s long term growth. We maintain our BUY recommendation on SUN with an FY26E intrinsic value of LKR 37.00.

Discussion (0)

Latest Reports

Free

Related Reports

Free

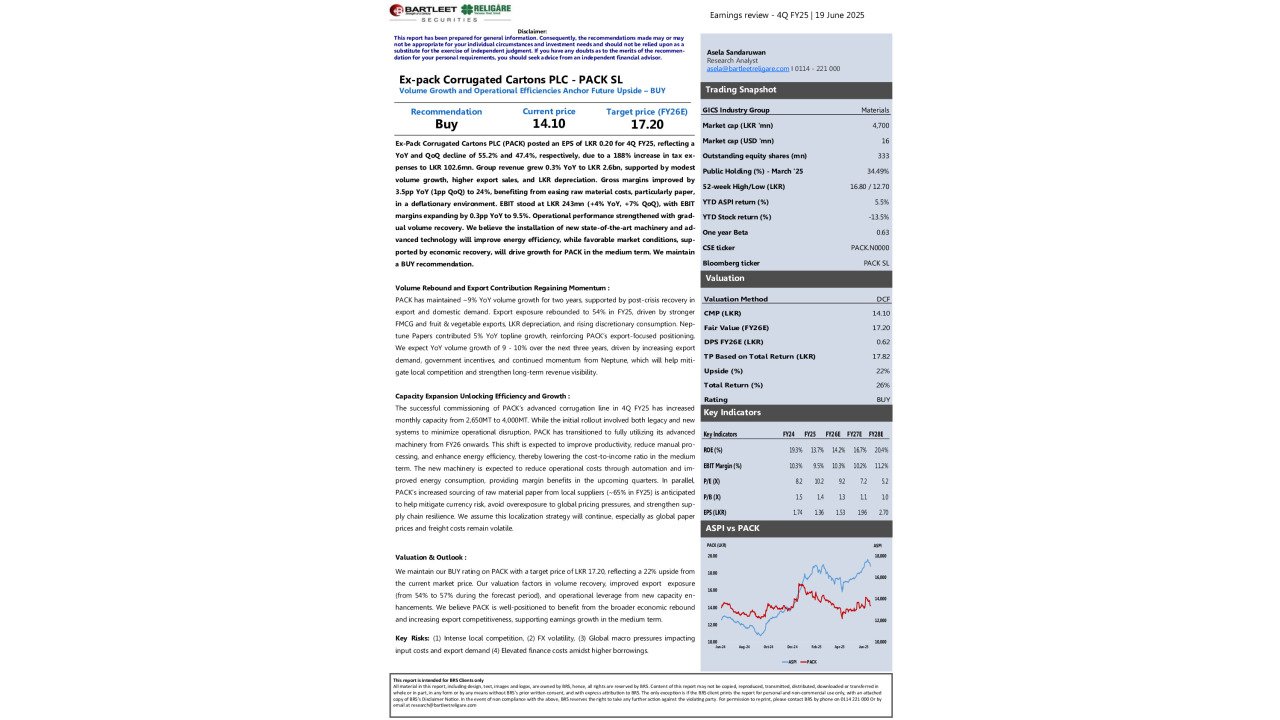

Ex-pack Corrugated Cartons PLC (PACK) - ...

Ex-Pack Corrugated Cartons PLC (PACK) posted an EPS ...

513

0

You must login to post a comment.