ACL 3Q FY26 Earnings Review - BRS Equity Research

Loading...

Earnings Reviews

19/05/2026

277

0

ACL Earnings Review – 3Q FY26

📈 3Q FY26 Performance: EPS increased to LKR 2.57 (vs LKR 1.53 YoY), supported by 29% revenue growth driven by higher volumes, while pricing remained broadly stable.

📊 Margins: Gross margin declined to 26.9% due to elevated raw material costs, while EBIT margin remained stable at ~21%, supported by higher revenue and other income.

📘 Outlook: Recent price revisions and a strong order book provide earnings visibility over the next two quarters, while further price adjustments may be required amid rising inflation, currency depreciation, and elevated input cost pressures.

Valuation & Recommendation: BUY | TP: LKR 134.60 (+36.5%)

Discussion (0)

Latest Reports

Free

Related Reports

Free

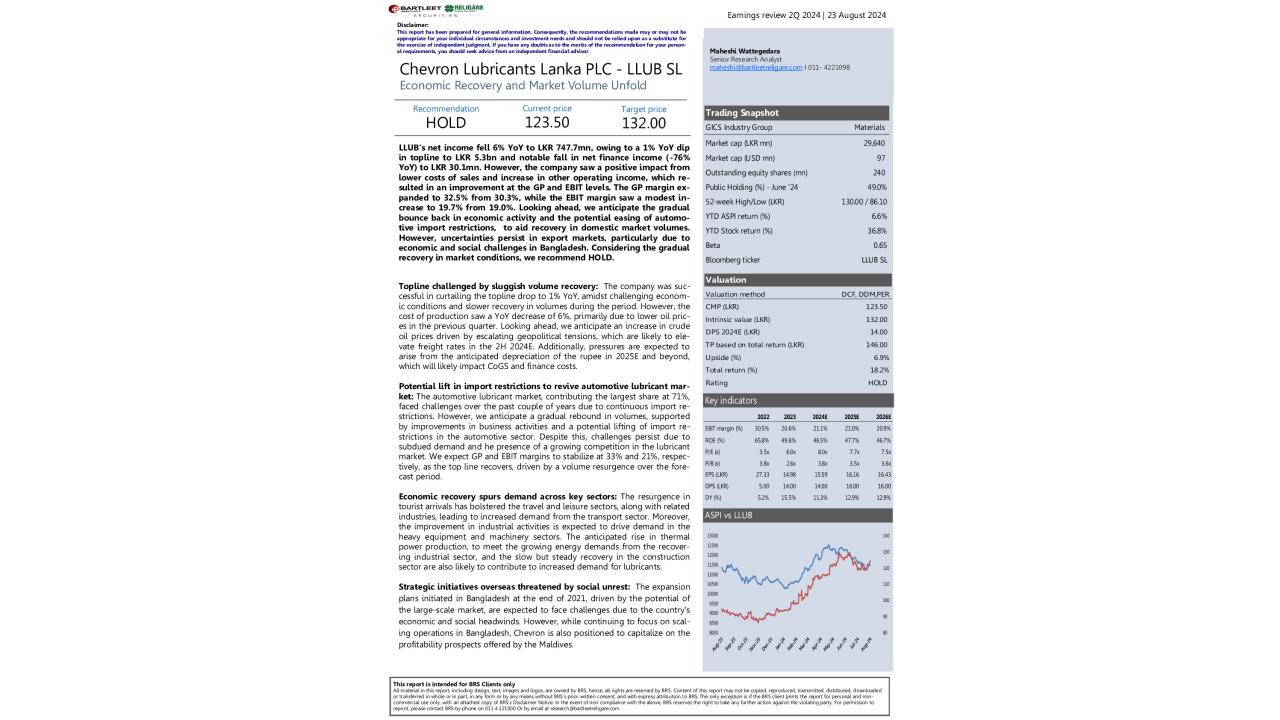

Chevron Lubricants Lanka PLC (LLUB SL ...

Economic Recovery and Market Volume Unfold LLUB's net ...

416

0

You must login to post a comment.